Small Business Loans

The best small business loans in Australia – A detailed guide to understanding and comparing the top small business loans.

$5K - $1M

Amount

3 months - 5 years

Term

From 1.33% p.m

Interest Rate

The best small business loans in Australia – A detailed guide to understanding and comparing the top small business loans.

As a small business owner, regular cash flow is a major factor that defines the health of your business. In order to maintain a steady cash flow to meet regular business challenges, small business owners like yourself often need to borrow money. While there are a lot of options available in the market, it is important to understand which is the right one for your business. In this page, we have tried to explain in simple terms the various loan options available to small business owners and how you can approach the right lender to secure your loan.

All about Small Business Loans

A definitive guide to small business loans – understand the different types of loan, compare them and choose the right one for your business in 2023.

What is a small business loan?

A small business loan, as the name suggests is a loan that is available to small and medium enterprise that are looking for funds to manage and grow their business. The loan is available for a predefined term and the repayment of the loan amount and interest is done in a systematic repayment method (weekly, fortnightly or monthly) till the amount is fully paid up. It is also called as small business finance, short term loans, small business funding etc.

The loan can be secured or unsecured, based on whether the loan is given against a collateral or security or based on the health and wealth of your business.

| Secured Loans | Unsecured Loans | ||

|---|---|---|---|

| Definition | These loans are given to small businesses against security, (usually a property, vehicle or another asset) which can be used to recover the loan amount in case of a default. The value of the secured asset is usually higher than the loan amount provided to reduce the risk for the lender. | These are loans that are provided to small business owners based on their turnover, credit history, and purpose. No collateral or security is taken against an unsecured loan and the amount provided by the lender is usually up to 100% of the average monthly turnover of the business. The risk is usually higher for the lender in case of unsecured business loans. | |

| Pros |

|

|

|

| Cons |

|

|

|

What is the best loan for my small business?

Every business is unique and so are the business challenges. Hence, there is no one loan that fits best for any business or category. The best way to approach a small business loan is to take a structured approach by answering some of these questions below.

1. What can I use the business loans for?

A strong action plan: The primary question one must ask is, why do I need this loan? List the outcomes you intend to achieve with the loan, be it for buying new machinery, hiring more staff, inventory or simply working capital. Once you have a good reason and an action plan, you will have better clarity on how to utilise the funds.

2. How to choose the right lender for my business loan?

Identify lenders who cater to businesses like yours: There are a lot of lenders in the market and each of them have specific criteria on who they can fund, how much they can fund, documentation required and interest rates. Since businesses are different, lenders also have preferences on the type of businesses they cater to. Hence, it is important to identify the right business lending firm for your loan.

3. How can I repay the business loan?

Repayment Plan: Since you are applying for a loan, the lender must be convinced that you have adequate continuous business to ensure repayment of the loan. So, build a robust repayment plan that showcases your monthly income, overheads and loan repayment to convince the lender that your business is in good health. Your credit score will also play an important part here. If you don’t have a healthy score, you might not qualify for a loan or end up paying a higher interest rate. Use our Loan Calculator to check your approximate repayment amounts.

Also Read our blog on 7 effective steps to manage your small business loan repayments.

4. What documents should I submit to secure a loan?

Documentation: This is a critical (and often underestimated) part of the process that is vital to your loan’s approval. As mentioned above, every lender has a different criteria with respect to the loan they provide, and hence it is important that you are aware of and prepared to submit the necessary documents to ensure success of your application. This could include your business and personal tax returns, financial statements, bank statements and other legal documents related to your business.

Besides this, the basic minimum business loan eligibility criteria for a small business is outlined below.

- Active ABN with minimum 6 months in business

- Minimum turnover of $5000 per month

- Fair credit history

Once you have answered these questions satisfactorily, you can proceed to secure a small business finance.

The top small business loans in Australia - 2023

Compare the various types of loans to small businesses in Australia and choose the one that suits your business needs.

If you are a small business owner, today you have a host of options when it comes to business loans. But more options create more confusion. How does one choose the right loan to meet a business need? In this section, we have listed out the various options that are available to you as a business owner so that you can identify the one that suits your requirements best.

Unsecured Business Loans

An unsecured business loan is one, which does not require the borrower to pledge an asset or collateral against the debt. This is also one of the most popular type of business loan that is available to small businesses.

These loans are provided purely on the basis of performance of the business over a certain duration. This requires the borrower to show a consistently good credit rating, an excellent financial track record and adequate cash flow forecast. Since the bank or lender takes a higher risk in providing these business loans, the interest rate associated with these loans are also often higher.

These loans are offered for shorter periods ranging from 3 months to about 3 years and the loan amount varies from AUD $5000 to more than $500,000 depending upon the turnover of the business. Usually, lenders fund up to a maximum of 100% of the monthly revenue of the business.

What can I use this loan for?

Since unsecured business loans are available for smaller amounts and shorter durations, most small companies use them for their regular cash flow or working capital requirements. These could be for purchasing stock, buying a new equipment, hiring staff or even marketing.

Advantages and disadvantages

| Advantages | Disadvantages |

|---|---|

| No risk to personal assets or property | Higher Interest Rates |

| Funds available in quick time | Shorter loan tenures |

| Flexible repayment options | Amount based on monthly turnover |

Read more about Unsecured Business loans

Secured Business Loans

When businesses seek a loan pledging their property or any other assessable asset as security, it is referred to as Secured Business Loan. The assets you pledge to seek loans are often called collateral or security. You can use your residential property, commercial property, vehicles or machinery as security.

Secured Business Loan is provided for a fixed period of term, within which you need to repay the loan with agreed interest to reclaim your pledged asset. Because the loan is backed by collateral, the lenders tend to charge lower interest rates and provide the loan for a longer period of time compared to other business loan products. It is also considered less risky for the lender, as they can recover from potential losses in case of delinquent clients by taking possession of the asset.

What are the criteria for a secured business loan?

One of the most critical aspects of this loan is the asset you pledge against the loan. The lender will assess whether the asset is valuable enough to cover the value of the loan in case of default. Apart from assessing the asset’s value, they will also evaluate the overall health of your business and in order to do so, they would seek certain documents as listed below:

- Complete details of any income generated by the asset

- Copies of documents confirming the asset’s sale and transfer to prove ownership

- Details of an existing loan over the asset, if any.

- Copies of registered documents if any, that certifies the valuation of the asset

- Copy of insurance policy on the asset

Advantages and disadvantages

| Advantages | Disadvantages |

|---|---|

| Lower interest rates | Needs a security or collateral |

| Longer repayment period | Early repayment fees |

| Higher loan amounts | Risk of losing your asset |

Read more about Secured Business loans

Line of Credit

A business line of credit(LOC) is one where the lender grants access a amount to a business. However, no interest is incurred on the funds until they are tapped into. Unlike secured or unsecured loans, business line of credit can be utilized by the business when they choose to. The interest is paid only on the utilized funds and the balance funds are available for use later.

For instance, if the total approved line of credit is $50,000 and $25,000 is tapped into, access to the balance $25,000, if necessary, remains. If the utilized amount of $25,000 is paid back, there is access to the entire $50,000 without having to reapply, which is one of the biggest benefits of line of credit.

A business line of credit can be unsecured (without a collateral or security) or secured (typically, by inventory, receivables or other collateral) depending upon the health and wealth of your business. Lines of credit are often revolving and can be tapped into repeatedly.

The funds available with business LOC is usually lower than other typical loans available to small enterprises. Hence these funds are mostly used for immediate expenses like cash flow, working capital or for buying stock.

Typically, business lines of credit are more suited for businesses that have been for longer, have a higher credit score and a stable monthly turnover.

Does my business qualify for a business line of credit?

Any business that needs a continuous influx of funds qualifies for a business line of credit. Listed below are some scenarios to understand the qualification criteria better.

- Businesses that want flexible funding solutions

- Small businesses looking for quick funding options

- Businesses without any asset and collateral to avail secured loans

- Businesses with lower credit scores

Advantages and disadvantages of business line of credit

| Advantages | Disadvantages |

|---|---|

| Once approved, funds can be tapped into anytime | Chances of line of credit withdrawal at any time |

| Use only required funds from approved amount | Monthly interest repayment and additional fees applicable |

| Higher loan amounts | Risk of losing your asset |

Read more about Business Line of Credit

Equipment Finance

Business loans in Australia are purely need based. As a small business owner, when you are looking to purchase a piece of equipment for your business, including vehicles, machinery or technology, you look for small business loans for the same. This type of finance is called equipment finance or asset finance.

The types of equipment finance differ with how you procure the equipment for your business. For example, you might want to hire the equipment for a particular period of time, in which case, the lender becomes the owner of the equipment. If you are buying the equipment with the short-term loan, the bank/lending organization uses the asset as a security or collateral.

The types of equipment finance differ with how you procure the equipment for your business. For example, you might want to hire machines used in manufacturing for a particular period, in which case, the lender becomes the owner of the machines. If you are buying the machines with the short-term loan, the bank/lending organization uses the asset as a security or collateral.

How does equipment finance work?

Loan applied to purchase an equipment or asset for the improvement or growth of business is referred to as equipment loan. It could be anything that helps in the business, such as machinery, vehicle, computers etc. As it is applied for an asset, the asset becomes collateral or security in this case. The payment would include interest and principal over a fixed term, failure to pay the same could result in repossession of the equipment or any other asset kept as security by the lender.

Advantages and disadvantages of equipment finance

| Advantages | Disadvantages |

|---|---|

| Lesser documentation to secure funds | Higher interest rates than other loans |

| Equipment purchased can be used as security for loan | Cannot resell equipment till loan closure as the asset is owned by lender |

| Loan can be secured even if you have outstanding debt | Early repayment fees applicable during the loan tenure |

Read more about Equipment Finance

Invoice Finance

Of the various short-term loans available with banks and lenders, invoice finance is a kind in which businesses use their invoices to unlock cash thereby speeding up cashflow. They do this by selling their invoices to a third party in exchange for some advance cash the invoice is worth.

It is a way for SMEs to take a loan against the amount due from their customers. Not only does it help improve your cash flow, pay your employees and suppliers, it can also be reinvested in operations earlier, rather than waiting for the customers to pay their dues.

Who can benefit from an invoice finance?

Invoice small business loans for startups can benefit small, large and seasonal businesses alike. Small companies face money crunch due to late payments by clients or customers and invoice financing can bail them out of such tricky situations and ensure they get paid on time. Large businesses use invoice financing as a cash flow tool to remain unaffected by late payments and ensure smooth operations. Though cash flow is important for all kinds of businesses, it is particularly true for seasonal businesses wherein invoice financing can help their payments flowing even during seasonal lulls.

Advantages and disadvantages of invoice finance

| Advantages | Disadvantages |

|---|---|

| Cash available against pending invoices | Higher interest rates than other loans |

| Reduced risk of unpaid invoices | Reduced value of invoices |

| Quick access to funds | Non repayment by client can affect credit score |

Read more about Invoice Finance

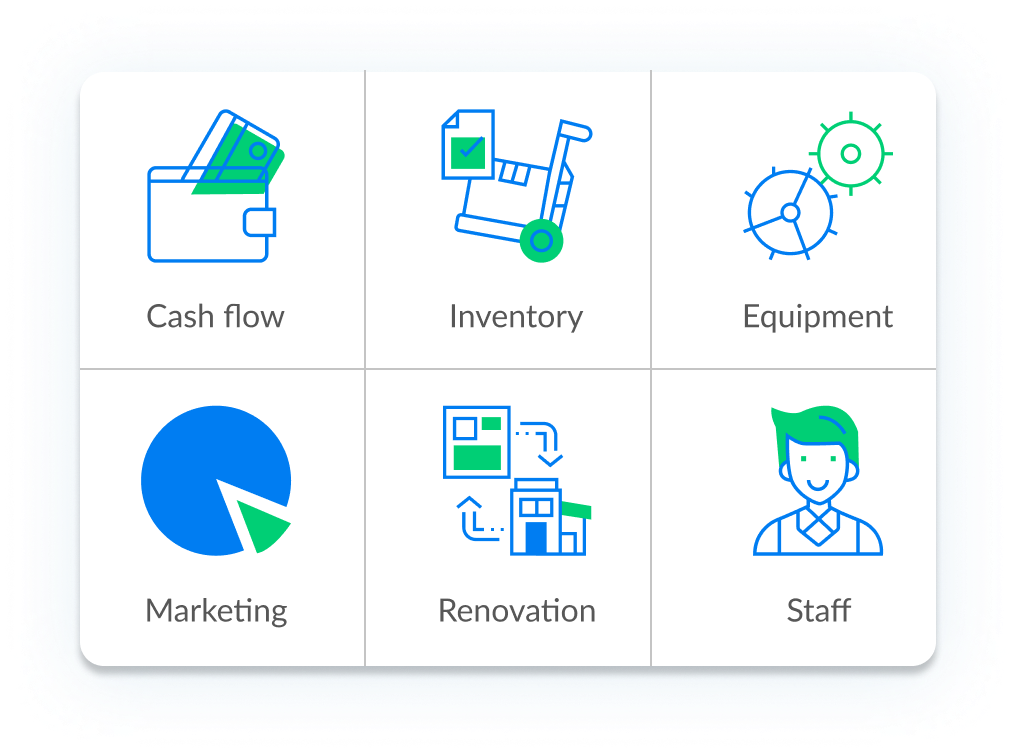

What can I use a small business loan for?

A small business loan can be used for any business purpose. Generally, lenders would be interested to ascertain the reason for the loan so that they know it’s used for business purposes only. However, it’s perfectly fine if you want to use the funds for multiple business purposes. Listed below are some of the common reasons funds are secured.

Want to see how other SMEs are using funds to grow their business? Read some of the Success Stories shared by our customers.

How to choose the right lender for my small business?

Once you have decided to go for a small business loan, the critical question arises – Which is the right loan for my business?

Small enterprises often struggle to identify a lender for their business needs. With each lender having a different criteria on the loan amount, terms and interest rates, it is confusing for businesses to identify a lender that will suit their business loan requirements. Here are a few factors that can help you identify the right lender for your business loan needs.

1. Reputation of the lender

Are you seeking the loan from a reputed lender? Are they transparent in their transactions and approach? Do they clearly state the terms and conditions to you before your loan is processed? Are there any hidden charges? These are probably some of the factors you must consider while ensuring you are dealing with a reputed lender to secure your loan.

2. Does the lender cater to your industry?

Each lender has a different appetite for risk and caters to different industries based on that. Hence, it’s quite possible that the lender you approach might not have your industry on the top of its list. It is important that you identify a lender that caters to the business you are in. This will considerably reduce the chances of rejection.

3. Compare lenders and loan terms

Once you have identified a couple of lenders you want to apply with, do a bit of background work on what they offer, their rates and terms. This will help you decide the various factors that matter to you and evaluate which is a better suited lender for that particular loan requirement.

A reliable way to compare loans is to compare the annual percentage rate (APR). APR is expressed as a percentage that represents the actual yearly cost of funds over the term of a loan. This includes any fees or additional costs associated with the transaction but does not take compounding into account.

4. Apply through a loan intermediary

If you are unsure which lender will be ideal for your loan need, it is advisable to look at business financial brokers or intermediaries online to find the right lender for your needs. When you do this, make sure you get to speak to an expert at the firm to understand how they can add value to your loan process.

At Capital Boost, we speak to all our clients in great detail to understand their business loan needs and then match them to a lender. Our knowledge of the different lenders’ criteria along with our understanding of our clients’ business helps us match our clients to the best fit lender. This helps us deliver exceptional value and outcome for our clients.

Top 12 reasons your business loan can get rejected and tips to overcome it.

Of all the small and medium enterprise that look for a funding in Australia, only 50% of them manage to secure funds to run their business. There are various factors that contribute to rejection of loans for the balance 50% of small businesses. Listed below are some of the common reasons why small businesses fail to secure funds.

If your loan application too has been rejected, identify the root cause for the rejection and take correct actions to ensure that you secure the loan your business needs.

1. Your business is relatively new

This is one of the main reasons why most new companies and start-ups fail to secure a funds for their business. Most lenders require you to be in business for a minimum of 6 months with a steady turnover. Since the funds are mostly unsecured, the risk is considerably higher for the lender if your business is not stable.

Tip: There is nothing much you can do here other than wait for your business to meet the minimum threshold criteria. Alternately, if you are desperate for funds to get your business going, look for smaller amounts from family and well-wishers to invest in your company instead.

2. Your business is not registered in Australia

Most lenders require your business to be registered in Australia with a valid ABN/ACN. This is one of the minimum criteria for your loan application to be considered.

Tip: If you are looking for a business loan, then ensure that your business has an active ABN for over 6 months. If not, you might have to wait till you satisfy this criterion.

3. Credit history

A relatively poor credit score can be a key reason why your business loan gets rejected. Different lenders have varying appetite for risk and hence this could vary from lender to lender.

Tip: If you have a poor credit history, ensure that you work towards improving it before you apply for any business funding . Also, you should approach lenders who have a bigger appetite for risk and are willing to fund your application despite a relatively poor credit score. Of course, your repayment amount might be higher in such cases since the lender has a higher risk.

4. Revenue of the company

Most lenders need you to have an average minimum turnover of $5000 per month for them to process your loan application. This is to ensure that you have adequate cash flow to be able to sustain your business and loan repayment.

Tip: Most lenders will look at your bank statements to ascertain your company’s turnover. If you have a cash component to your business, then ensure you file your BAS and submit the statements along with your bank statement to secure your loan.

5. Previous loan payment defaults

Defaults in debt repayment – either paid or unpaid can hamper your prospects for future loans and could also affect your credit score adversely.

Tip: Ensure that you do not default on your repayments and secure only funds that you can utilise effectively to drive more revenue for your business. If you have any pending defaults, repay those and work on improving your credit history before you look for a fresh funding.

6. Existing loans

Most small business finance lenders will fund you up to a maximum of 100% of your monthly turnover. So, if you already have existing loans, it’s unlikely that you will be able to secure a fresh loan exceeding your monthly turnover.

Tip: If you have already exhausted your business loan limit, you could look at secured business loans or a personal loan to secure additional funds for your business.

7. Lack of collateral/security

Secured business finance are often preferred by SMEs since these attract lesser rates of interest. However, if you do not have adequate security or collateral, lenders often reject the loan application.

Tip: Go for an unsecured business loan when you do not have or want to pledge an asset or collateral against the loan. The interest rates are higher for an unsecured loan, but then the risk is also minimal.

8. Lack of a business plan

When applying for a business funds, you need to convince the lender the purpose of the loan and how you intend to utilise the funds. Since these loans are meant for business purpose, it is important for the lender to know how you plan to utilise the loan amount in a meaningful way to meet your business objectives.

Tip: Identify your purpose of applying funds and be transparent with the lender on the purpose of the funds and how you will use the funds to grow your business. This could be for working capital, purchasing stock, company vehicles, machines, marketing, hiring new staff or any other related business purpose.

9. Your industry is considered ‘risky’ by lenders

If you are in a high investment or low margin business, some lenders are apprehensive of approving funds. This is often because of past experience with clients from similar industries or businesses. While this is not a reflection of your business or repayment capability, it could often lead to your business not securing a loan.

Tip: Identify lenders who cater to your industry. Speak to peers within your industry or to a business loan broker to identify lenders whom you can approach for your business loan.

10. Incomplete or insufficient paperwork

The paperwork required to secure a small business finance is considerably lesser compared to securing a loan from a tradition bank. However, if you don’t have the adequate paperwork that can help lenders evaluate your business and repayment capability, it is difficult for them to approve your funds. Hence, have your documents and paperwork in place before you apply for a small business loan.

Tip: In most cases, lenders seek your latest bank statements, business activity statement (BAS), driving license and similar documents. Keep these handy so that you can go through the approval process faster.

11. The loan type is not suited to your business

There are various types of small business finance. You might or might not qualify for a loan based on the type of the loan and your business. It is important that you understand the loan details before you apply for the right one.

Tip: Read about the various types of loans and understand which one best suits your requirement. Alternately, apply for a loan with us and one of our lending specialists will get in touch with you to understand your requirements and find the right lender for your loan requirement.

12. You have not approached the right lender

Different lenders have different criteria for approving funds. This could be with respect to turnover, industry, loan amount, interest rates, etc. It is important that you reach out to the right lender for your loan. Else you might face rejection on your application and lose time and money both in the application process.

Tip: This is where you can take the help of an intermediary like us. Having partnered with all leading lenders in Australia, we understand their criteria and terms and based on your business, will match you to a lender that best suits your requirements.

Reviews

Frequently Asked Questions

Here are the top 10 frequently asked questions with respect to small business loans.

Does my business qualify for a small business loan?

How much money can I borrow for my small business?

How can I apply for a small business loan?

How long does it take for the loan to be processed?

What are the documents I need, to secure a small business loan?

Why should I submit my bank statement to secure a business loan?

What happens if I don’t repay my small business loan on time?

Can I get a small business loan with a bad credit?

Why should I secure a loan through Capital Boost?

Contact Us

At Capital Boost House, we understand your need to grow and are committed to your success.

Speak to us today

To know more about our offerings and how you can get your business loan at the earliest, reach out to us!

Got a query? Reach out to us

Needless to say, your contact details are safe with us and we assure you that your data will not be misused.